Buyers Intro

Home Buying

Buyers Intro

Home Buying

So You Want to Buy a Home?

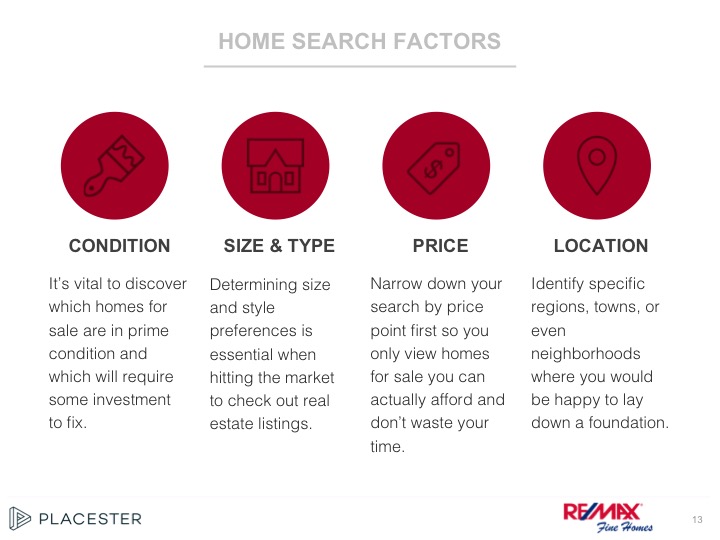

Whether you are a first time home buyer or you are buying your 4th rental property - the process can be overwhelming and simply stressful. Buying a house can be one of the biggest purchase decisions you may make. There is no reason you have to go it alone. With a licensed real estate agent you will have someone by your side during the entire process from the property search for the right house and making an offer to negotiating the terms and getting you to the closing table. Click a link below to find the following buyer resources:

Nashville Property Search

Get Email Alerts

Buying a Home

Nashville Neighborhoods

Home Buyer Tips

Home Buyer FAQs

Nashville Property Search

Nashville Property Search

Nashville Property Search

Nashville Property Search

Nashville Property Search:

- $3 Million homes - $75,000 condos - 10 bedroom mansions - 1 bedroom lofts - properties with 5 stable barns - homes on 127 acres - 23,000 square feet of warehouse space -

Click the link below to start your search right now - no matter what you are looking for!

Home Buyer Email Alerts

Home Buyer Email Alerts

Home Buyer Email Alerts

Home Buyer Email Alerts

Home Buyer Email Alerts:

Want to see new homes for sale in Nashville, Tennessee? Fill out the form below and I will set you up to receive email alerts via RealTracs, our local multiple listing service (MLS). What does that mean? You will receive regular updates for new homes to hit the market that fit your individual needs. You will only receive an email when a home that meets your criteria is new to the market or decreases in $1000 or more. You can be vague, "I want to buy a home in Nashville under $300,000; or you can be as specific as you like, "I want to buy a home in Inglewood with 1,500 square feet, 3 bedrooms, a 2-car garage and a swimming pool"

Trulia and Zillow can be great resources to find general market information as well as home buyer tips and home seller tips but I find the listed homes are often under contract or have already closed. This can be very annoying for serious home buyers conducting a property search. Whether you are actively looking to buy a home in Nashville or simply tired of inaccurate listing information, I am happy to set you up to receive regular updates via email. Click the button below to tell me about the home you want to purchase.

Buying a Home

Buying a Home

Buying a Home

Buying a Home

Buying a Home:

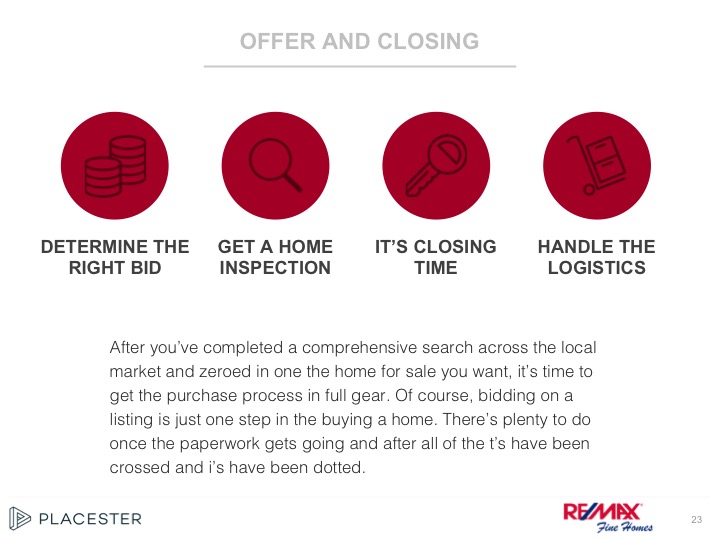

Buying a home can be fun and exciting but it can also be a daunting task. Home buying is more than swiping right on your phone and attending to open houses. Even if you found your dream home at an open house you still have to line up the funding, navigate the contracts, write a competitive offer, meet with inspectors and appraisers, negotiate repairs and get to the closing table. Whether you are a first time home buyer or just want to know how to buy a home the slides below will give you a taste of what to expect.

For more information on how to buy a home - contact me today.

Nashville Neighborhoods

Nashville Neighborhoods

Nashville Neighborhoods

Nashville Neighborhoods

Nashville Neighborhoods:

- Your guide to Nashville neighborhoods is coming soon! -

Home Buyer Tips

Home Buyer Tips

Home Buyer Tips

Home Buyer Tips

Home Buyer Tips - Top 10

Home Buyer Tip #1: Research Is The Key To Discovery

Home sellers won't call you with an offer to buy a maintenance-free home with a wonderful mortgage. You have to find the gems yourself! Only by reading available materials, talking to friends and experts, and spending time looking at different homes, schools, and neighborhoods will you end up with your American dream. Avoid the nightmares by learning how best to buy and maintain a home.

Home Buyer Tip #2: Make A Plan And Get Pre-Qualified

Every important decision needs to be clearly thought out. Developing a home buying plan can help you focus on the important factors and organize the entire process. You may even want to use a binder with sections on house hunting, home financing, service providers, etc. Loan pre-qualifying helps you determine the home price you can afford and presents you as a genuine prospect to the seller. A lender typically uses the 28% formula (your monthly mortgage can't exceed 28% of your monthly income) in approving your loan. Planning your actions and getting pre-qualified will keep you out of the panic mode and allow you to take advantage of opportunities. A thorough plan will save both time and money!

Home Buyer Tip #3: Value, Value, Value

The days of 10-30% annual appreciation have passed. Homebuyers in the 1970's benefited tremendously from what seemed like ever appreciating home prices. Nowadays, you're looking at slow growth while guarding against the possibilities of falling prices, skyrocketing ARM rates and corporate layoffs that can dramatically affect your home values. The classic rule of buying the worst house in the best neighborhood still applies. If you buy with an eye towards improvement, you can customize the home to fit your needs. The saying, "make money buying a home, not selling one," should keep you focused on the long-term importance of the purchasing price.

Home Buyer Tip #4: Create A Top 10 List Of Amenities

When shopping for a home, list the features (fireplace, fenced-in yard, new appliances, etc.) that are most important to you in deciding on which home to buy. Establishing "your criteria" early on will save time shopping for inappropriate homes and may keep you from buying a home on a whim. As detailed in Tip #3, your top reason for buying a home should be the value you are getting. Some of your top 10 amenities should logically be sacrificed if an incredible value is available.

Home Buyer Tip #5: Fixed vs. Adjustable Rate Mortgages

Adjustable rate mortgages have an initial fixed rate, which is followed by a period of adjustment intervals during which the rate adjusts based on the performance of several key indexes. Typically the initial fixed rate on an ARM is slightly lower than the comparable rate of a fixed rate mortgage. Fixed rate mortgages allow buyers to take out a long term loan without having to worry about changing interest rates or monthly payments. Most fixed rate loans are offered in either 15 or 30 year terms. Most buyers will be well served by a fixed rate loan, but each situation is unique. While ARM loans have become less popular in recent years, they can still be a viable option for some buyers - especially those who plan on selling again in the short term.

Whichever loan you choose; make sure that you scrutinize all the closing costs. If you are required to have a mortgage escrow account and private mortgage insurance, make sure you understand the terms and cancellation procedures (your Real Estate Agent has publications to assist you). Also, make sure there are no prepayment penalties so that you can utilize an accelerated mortgage plan. A good mortgage reduction plan can save you tens of thousands in interest costs, and shorten your loan term, with only small extra principal payments. If you experience negative changes in your job, health, or marital status, you can revert to the standard payments in your mortgage contract.

Home Buyer Tip #6: Sign A Contract That Protects You

Make sure that the contract you put on a house allows you to arrange financing, inspect the home and negotiate any problems that you uncover. Ensuring that the contract you sign will minimize potential legal battles will let you swim in your new pool with your family and neighbors instead of with the sharks.

Home Buyer Tip #7: Put Yourself In The Seller's Shoes

You are about to make one of the most important decisions that will affect both your life and the life of the seller. If you take time to understand the reasons the seller bought the home, their reasons for selling, and the home improvements they have or have not made, you'll be in a better position to evaluate the home and negotiate a better deal. In the end, the home buying process excludes the professionals and comes down to the individuals buying and selling the home. A closer look at the seller may help you in deciding whether and for how much to buy a particular home.

Home Buyer Tip #8: Develop A Mortgage Shopping Chart

One of the biggest decisions to make before putting a contract on a home is how to finance the purchase. There are 10,000 lenders competing for your mortgage business. The days of simply walking into the community bank and negotiating with the loan department manager are over. Today, you can apply for a loan over the Internet or even use a mortgage broker to shop for your loan with hundreds of lenders. When choosing a lender, you want to avoid apples to oranges contrasts by comparing fixed rates to fixed rates, not fixed to ARM's. Create a chart that lists different types of loans, fees, and at least five mortgage providers (including a mortgage broker).

Home Buyer Tip #9: Get A Quality Home Inspection

Although it is hard to believe, more people pay for inspections before buying used cars than when making the biggest investment of their lives - their homes. Paying for a qualified home inspection before you buy a home isn't just spending "a little extra" for peace of mind; it's absolutely essential for anyone who doesn't want to spend thousands of dollars for repairs.

Home Buyer Tip #10: Peace Of Mind: Home Protection Plans

To protect both you as a buyer, as well as the seller, it is a good idea to purchase a home protection plan. What exactly is it? A home warranty, or home protection plan, is a service contract, normally for one year, which protects homeowners against the cost of unexpected repairs or replacement of their major systems and appliances that break down due to normal wear and tear. A negotiable contract between the buyers and sellers which does not overlap or replace homeowner's insurance policy, this type of warranty can save the new homeowner lots of headaches, as well as put seller's fears to rest. The warranty covers mechanical breakdowns, while insurance typically repairs the related damage. For example: if a hot water heater burst and destroyed a wall in your home, the warranty would repair the water heater and your insurance would pay to fix the wall!

Home Buyer FAQs

Home Buyer FAQ's

Home Buyer FAQs

Home Buyer FAQ's

Home Buyer Frequently Asked Questions:

HOME BUYER FAQ #1: Why should I hire a Real Estate agent?

HOME BUYER FAQ #2: Are condos a good investment?

HOME BUYER FAQ #3: What rules and regulations do associations regulate?

HOME BUYER FAQ #4: What kind of insurance do I need?

HOME BUYER FAQ #5: What do I need to know about mortgages?

HOME BUYER FAQ #1: Why should I hire a Real Estate Agent?

- They will help you determine how much home you can actually afford. Often, they can suggest additional ways to accrue the down payment and explain alternative financing methods. They can also introduce you to a mortgage counselor and arrange to have you "pre-approved" which can improve your negotiating position and enable you to achieve your home-buying objectives faster and with less stress.

- Providing client level services, they can work for you as a buyer's agent and help negotiate the best price and terms for you. Or, they can serve as a seller's sub-agent (or disclosed dual agent), acting as a liaison between you and the seller to present offers and counteroffers until an agreement is reached.

- They will help you work out a realistic idea of the home best suited to your needs - size, style, features, location, accessibility to schools, transportation, shopping, and other personal preferences.

- They have access to a listing of all available homes in the multi-list system, can evaluate them in terms of your needs and affordability, and will not waste your time showing you unsuitable homes.

- They can often suggest simple, imaginative changes that could make a home more suitable for you and improve its utility and value.

- They can supply information on real estate values, taxes, utility costs, municipal services and facilities, and may be aware of proposed zoning changes that could affect your decision to buy.

- Although the law does not normally require an attorney to review documents or oversee real estate closings, they can provide you with a list of law practitioners to choose from if you would like to use the services of an attorney.

- They can help familiarize you with the closing process and they will obtain closing figures in advance of closing for your review.

- They can provide you with a list of qualified home inspectors, pest inspectors, surveyors, and help to coordinate inspection appointments.

HOME BUYER FAQ #2: Are condos a good investment?

Condominiums have held their value as an investment despite economic downturns and problems with some associations. In fact, condos have appreciated more in the past few years than when they first came on the scene in the late 1970s and early 1980s, experts say.

While there are lots of reports about homeowners association disputes and construction-defect problems, the industry has worked hard to turn its image around. Elected volunteers who serve on association boards are better trained at handling complex budget and legal issues, for example, while many boards go to great lengths to avoid the kind of protracted and expensive litigation that has hurt resale value in the past.

Meanwhile, changing demographics are making condominiums more attractive investments for single homebuyers, empty nesters and first-time buyers in expensive markets.

HOME BUYER FAQ #3: What rules and regulations do Associations regulate?

Typical covenants, codes and restrictions (CC&Rs), which govern condo associations, give the board authority to make and enforce reasonable rules for the use of common property. But that would not apply to interior spaces owned by smokers themselves.

A homeowners association's board of directors can restrict smoking if it applies to indoor common spaces such as hallways or recreation rooms. Outdoor spaces are a different story, say legal experts. Any restriction would probably hinge on local laws (i.e. if a city banned smoking outdoors, a homeowners association probably could restrict smoking in its outdoor spaces).

The 1990 Americans with Disabilities Act does not require strictly residential apartments and single-family homes to be made accessible. But all new construction of public accommodations or commercial projects (such as a government building or a shopping mall) must be accessible. New multi-family construction also falls into this category.

In all states, the Federal Fair Housing Act provides protection against discrimination for people with physical or mental disabilities. Discrimination includes the refusal to make reasonable modifications to buildings that aren't accessible to the disabled.

HOME BUYER FAQ #4: What kind of insurance do I need?

A standard homeowners policy protects against fire, lightning, wind, storms, hail, explosions, riots, aircraft wrecks, vehicle crashes, smoke, vandalism, theft, breaking glass, falling objects, weight of snow or sleet, collapsing buildings, freezing of plumbing fixtures, electrical damage and water damage from plumbing, heating or air conditioning systems, according to the Insurance Information Institute, a Washington, D.C.-based nonprofit group for the insurance industry.

Such policies are "all-risk" policies, which cover everything except earthquakes, floods, war and nuclear accidents.

A basic policy can be expanded to include additional coverage, such as for floods and earthquakes and even workers' compensation for servants or contractors. Home-based business-coverage, an increasingly popular rider, does not cover liability associated with the business.

Insurance experts recommend that homeowners obtain insurance equal to the full replacement value of the home. On a 2,000-square-foot home, for example, if the replacement cost is $80 per square foot, the house should be insured for at least $160,000.

For personal items, homeowners can increase their coverage beyond the depreciated value of items such as televisions or furniture by purchasing a "replacement-cost endorsement" on personal property.

Some experts recommend an inflation rider, which increases coverage as the home increases in value.

HOME BUYER FAQ #5: What do I need to know about mortgages?

The modern mortgage market offers a variety of mortgage loans catering to the needs of homebuyers. The titles and details of these plans can become confusing, especially as new types are introduced continuously. You can make sense of these loan types, however, if you understand the basic principles that govern all mortgage loans. Again, you can look to your real estate professional for assistance. I am happy to get you in contact with outstanding mortgage lenders who can walk you through each step of the mortgage process.

Basic Principles of all Mortgage Loans

- The home is used as security to back up the loan. A lender can force sale of the home if the borrower defaults by failing to make scheduled payments.

- The larger the loan compared to the value of the home, the more risky for the lender and, often, the more expensive the loan will be.

- Interest earned by the lender always is equal to the periodic interest rate times the outstanding principle balance of the loan. The periodic interest rate is the annual interest rate divided by the number of payments in the year (usually one per month).

- The required payment usually is a bit larger than the interest due so that some of the loan principal is repaid with each payment. This process is called Amortization and is why most mortgage loans can be retired when all the monthly payments have been made.

All mortgage loans have one of the following features:

- Fixed payment and fixed interest rate - fixed rate mortgages

- Fixed rate but variable payment - graduated payment mortgages

- Variable rate and variable payment - adjustable rate mortgages

As you learn more about the types of financing available, you will notice that some loans appear to have more favorable terms. That may indicate that those loans are, indeed, bargains (and it does pay to shop around), but usually it means that those loans could have some feature that is less appealing to borrowers. For example, shorter-term loans often have slightly lower interest rates compared to longer-term loans. However, the monthly payment for the same amount of principal may be higher because of the shorter term. Variable rate loans usually have much lower interest rates to compensate for the risk the borrower accepts that interest rates will rise in the future.